Over the past six months, Fastly’s shares (currently trading at $6.33) have posted a disappointing 14% loss while the S&P 500 was down 3.4%. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is there a buying opportunity in Fastly, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Even with the cheaper entry price, we're swiping left on Fastly for now. Here are three reasons why FSLY doesn't excite us and a stock we'd rather own.

Why Do We Think Fastly Will Underperform?

Founded in 2011, Fastly (NYSE:FSLY) provides content delivery and edge cloud computing services, enabling enterprises and developers to deliver fast, secure, and scalable digital content and experiences.

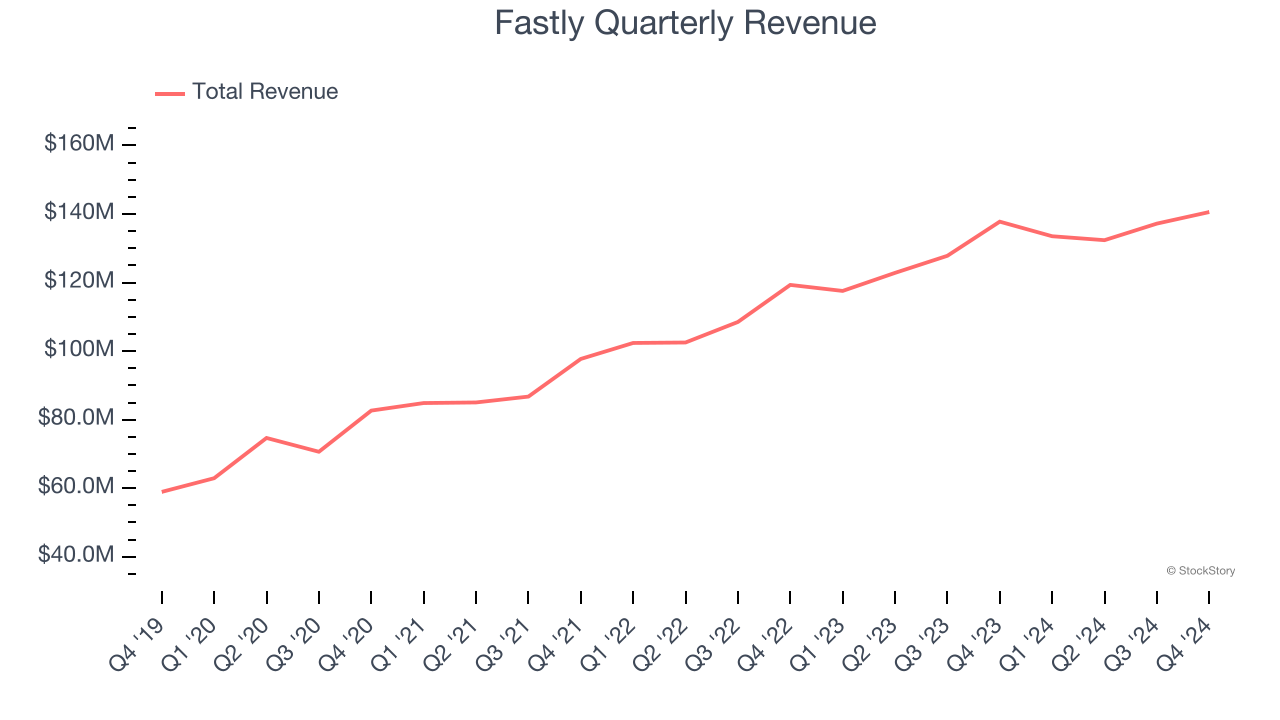

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Fastly grew its sales at a 15.3% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the software sector, which enjoys a number of secular tailwinds.

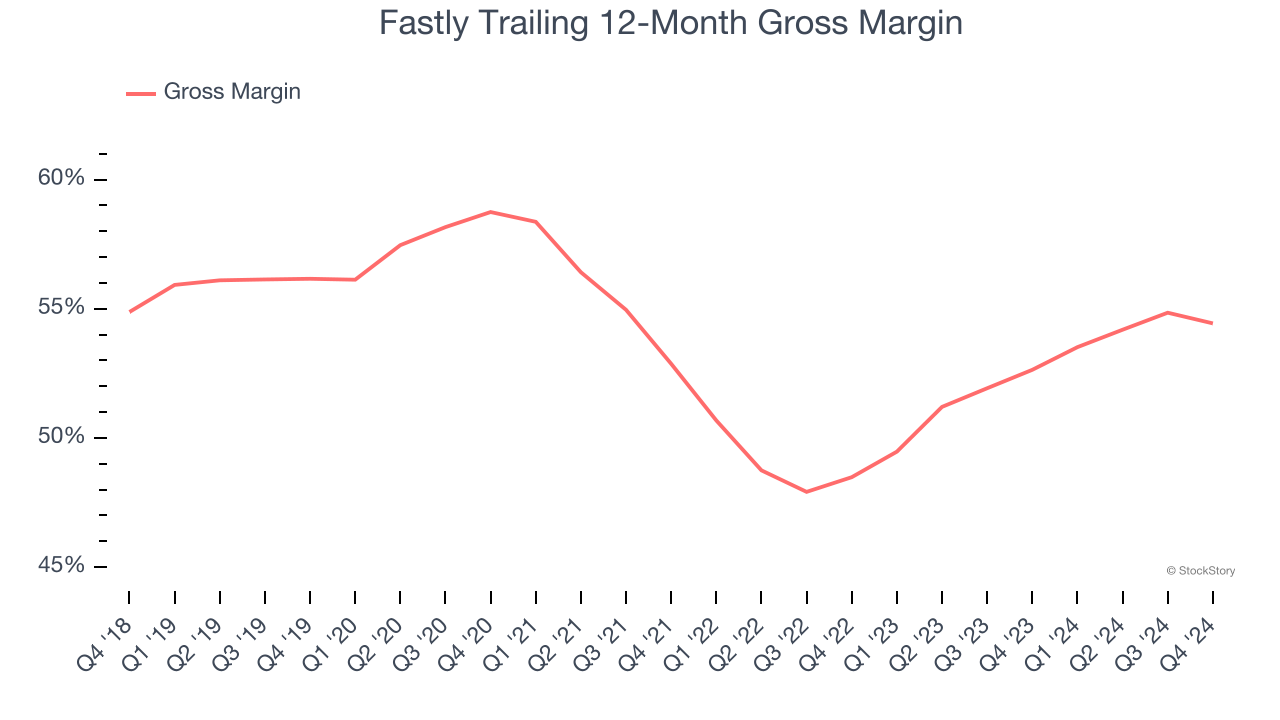

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Fastly, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Fastly’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 54.4% gross margin over the last year. Said differently, Fastly had to pay a chunky $45.57 to its service providers for every $100 in revenue.

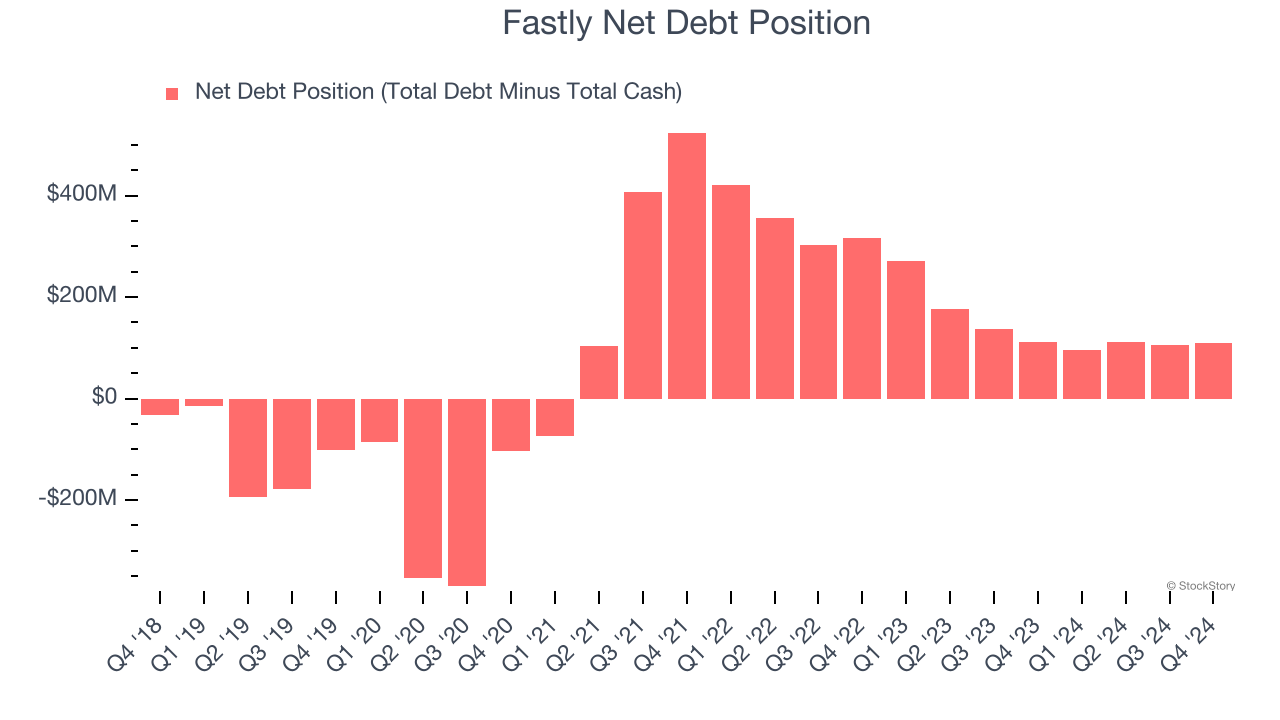

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Fastly burned through $35.74 million of cash over the last year, and its $404.7 million of debt exceeds the $295.9 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Fastly’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Fastly until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

Fastly doesn’t pass our quality test. Following the recent decline, the stock trades at 1.6× forward price-to-sales (or $6.33 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. There are better investments elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Fastly

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.