The end of an earnings season can be a great time to discover new stocks and assess how companies are handling the current business environment. Let’s take a look at how Campbell's (NASDAQ:CPB) and the rest of the shelf-stable food stocks fared in Q4.

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

The 21 shelf-stable food stocks we track reported a mixed Q4. As a group, revenues were in line with analysts’ consensus estimates while next quarter’s revenue guidance was 0.5% above.

In light of this news, share prices of the companies have held steady as they are up 2.5% on average since the latest earnings results.

Campbell's (NASDAQ:CPB)

With its iconic canned soup as its cornerstone product, Campbell's (NASDAQ:CPB) is a packaged food company with an illustrious portfolio of brands.

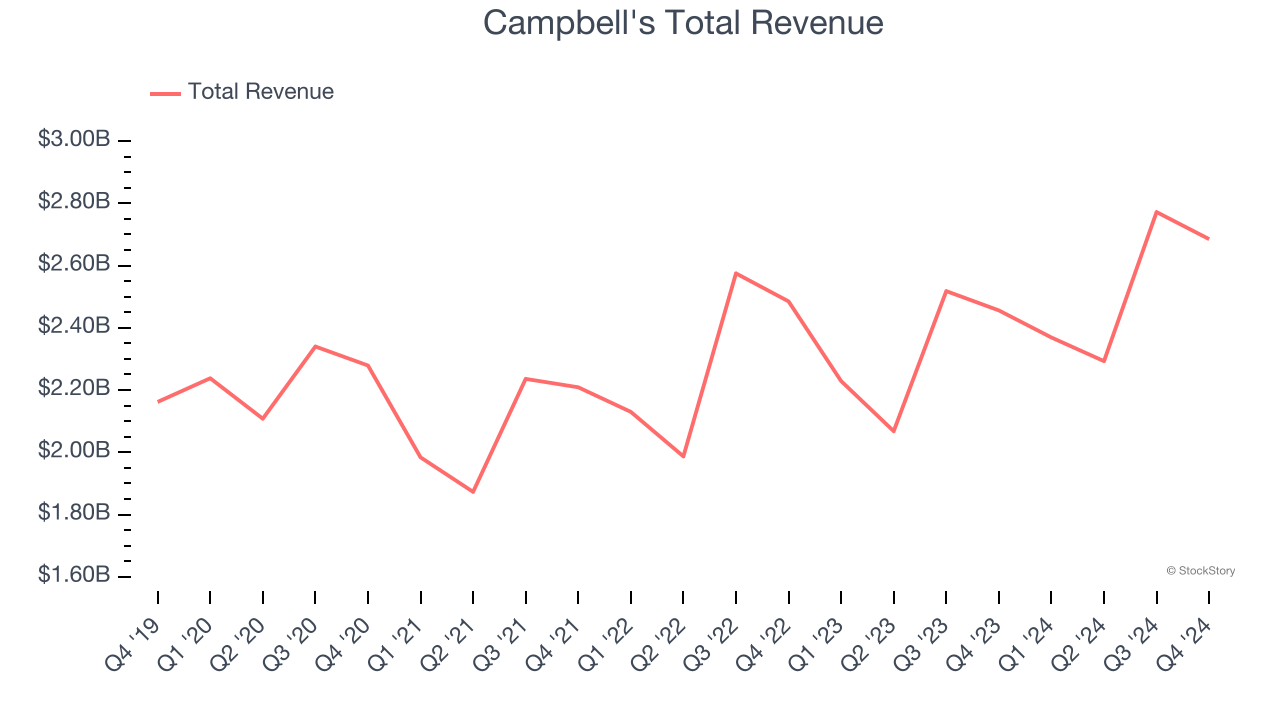

Campbell's reported revenues of $2.69 billion, up 9.3% year on year. This print fell short of analysts’ expectations by 1.8%. Overall, it was a slower quarter for the company with a miss of analysts’ organic revenue estimates and full-year EPS guidance missing analysts’ expectations.

The stock is up 3.6% since reporting and currently trades at $41.77.

Read our full report on Campbell's here, it’s free.

Best Q4: Lancaster Colony (NASDAQ:LANC)

Known for its frozen garlic bread and Parkerhouse rolls, Lancaster Colony (NASDAQ:LANC) sells bread, dressing, and dips to the retail and food service channels.

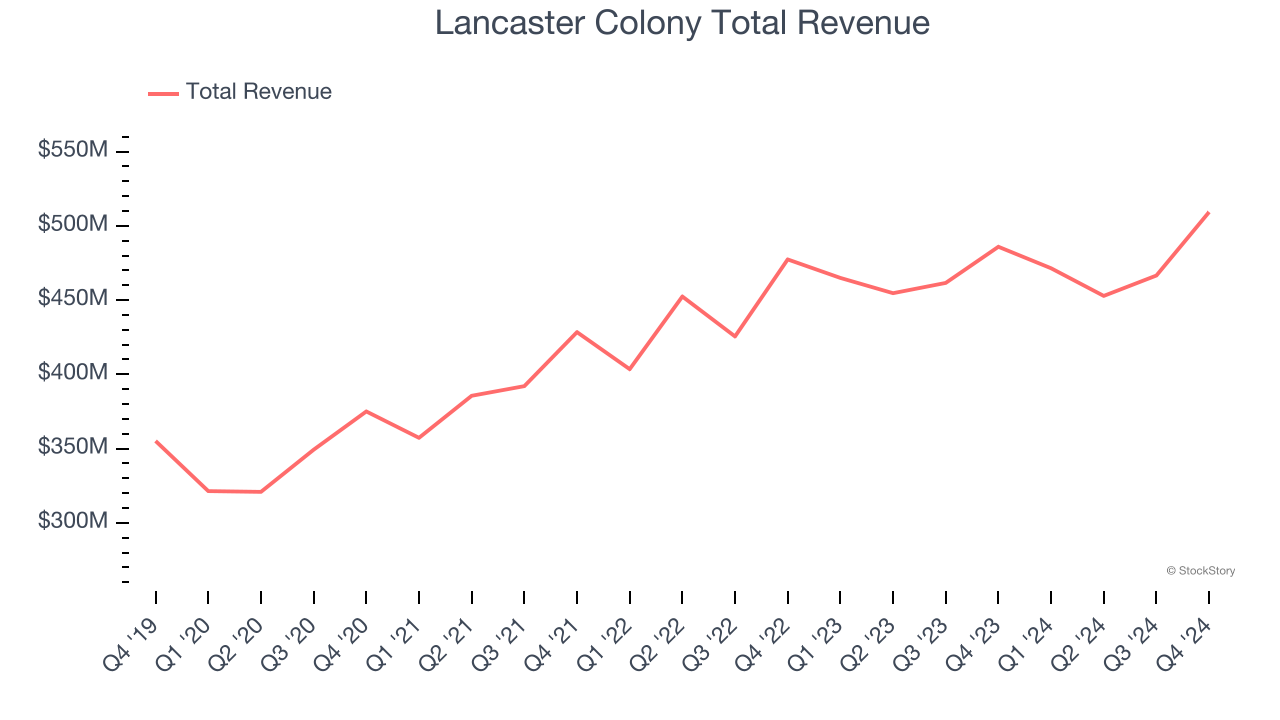

Lancaster Colony reported revenues of $509.3 million, up 4.8% year on year, outperforming analysts’ expectations by 2.8%. The business had a very strong quarter with a solid beat of analysts’ EBITDA estimates and an impressive beat of analysts’ adjusted operating income estimates.

Lancaster Colony achieved the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 14.7% since reporting. It currently trades at $190.99.

Is now the time to buy Lancaster Colony? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Lamb Weston (NYSE:LW)

Best known for its Grown in Idaho brand, Lamb Weston (NYSE:LW) produces and distributes potato products such as frozen french fries and mashed potatoes.

Lamb Weston reported revenues of $1.60 billion, down 7.6% year on year, falling short of analysts’ expectations by 4.3%. It was a disappointing quarter as it posted full-year revenue guidance missing analysts’ expectations.

Lamb Weston delivered the weakest full-year guidance update in the group. As expected, the stock is down 32.2% since the results and currently trades at $53.

Read our full analysis of Lamb Weston’s results here.

Utz (NYSE:UTZ)

Tracing its roots back to 1921 when Bill and Salie Utz began making potato chips in their kitchen, Utz Brands (NYSE:UTZ) offers salty snacks such as potato chips, tortilla chips, pretzels, cheese snacks, and ready-to-eat popcorn, among others.

Utz reported revenues of $341 million, down 3.1% year on year. This print came in 2.2% below analysts' expectations. Taking a step back, it was a satisfactory quarter as it also logged an impressive beat of analysts’ EBITDA estimates but a significant miss of analysts’ gross margin estimates.

The stock is up 7.4% since reporting and currently trades at $14.44.

Read our full, actionable report on Utz here, it’s free.

J. M. Smucker (NYSE:SJM)

Best known for its fruit jams and spreads, J.M Smucker (NYSE:SJM) is a packaged foods company whose products span from peanut butter and coffee to pet food.

J. M. Smucker reported revenues of $2.19 billion, down 1.9% year on year. This number lagged analysts' expectations by 1.7%. More broadly, it was a mixed quarter as it also recorded an impressive beat of analysts’ gross margin estimates but a miss of analysts’ organic revenue estimates.

The stock is up 8.4% since reporting and currently trades at $118.38.

Read our full, actionable report on J. M. Smucker here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.